By Carr Mitchell on Jul 3, 2026 1:41:17 PM

Death Planning Solution for:

Married Couples/Civil Partners (estates valued under the tax free amount), And Non-Married couples (Any Estate Value)

If you do not have a valid Will when you die, your assets will be distributed in accordance with the Intestacy Rules, laid down in the Administration of Estates Act 1925 and the Inheritance & Trustees’ Powers Act 2014. The people that you would want to inherit your assets may not and your estate’s tax position could also be affected.

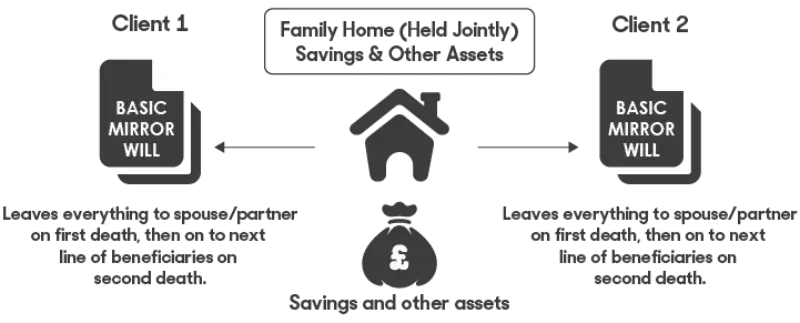

Typical Existing Planning

If you die without a valid will, or you have a basic mirror will in place, your assets could be exposed to the below risks after first death:

Following second death there are further risks to your assets that you want your loved ones to benefit from:

Our Solution

Sever the tenancy on the jointly owned family home and any other properties (if applicable), to become ‘tenants in common’. Equalise savings and investments into sole names rather than joint names.

Following first death, the deceased’s share of the assets are directed into their Discretionary Trust of Residue (which deals with their NRB & RNRB) via the Will. The surviving spouse or partner can continue to live in the family home and benefit from the other assets, and is still able to move house, if they choose to do so. In the event that the survivor enters care, the survivor’s assets only include a half share of the family home plus any other assets they own

Your beneficiaries have access to the trust funds but the trustees can ensure that these assets do not enter their beneficiaries estates and therefore are more protected from the following:

In some cases it may be beneficial to use multiple trusts. Multiple trusts can increase flexibility and autonomy, as it enables each beneficiary to have and be ‘in control’ of their ‘own Trust’. There are also various options open to trustees following death to try and reduce the impact of future tax charges in some cases.

This page contains only general guidance and is not to be construed as advice for any personal planning. Any planning should be based on bespoke advice tailored to your specific circumstances.

No Comments Yet

Let us know what you think